Fax: 07 5452 7301

Email: nathan@ffsolutions.com.au

Latest News

Magnificent Seven: More diverse than they may appear The Magnificent Seven are more diverse businesses than their shared label suggests

. The “Magnificent Seven.” It’s an understandable, memorable, and concise term, but its simplicity masks important distinctions. With the backdrop of strong U.S. stock market performance attributed to a handful of technology companies, the group’s run has fuelled questions about market concentration. When we look more closely, we see a clutch of U.S. stock market leaders that are more diversified than some may think.

The Magnificent Seven goes well beyond AIAlphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla offer a wide range of products and services, with some areas of overlap. Certainly, their activities extend well beyond AI. The companies have a diverse footprint across industries, variously functioning as global marketplaces, cloud computing providers, and even automobile manufacturers and physical grocery store operators.

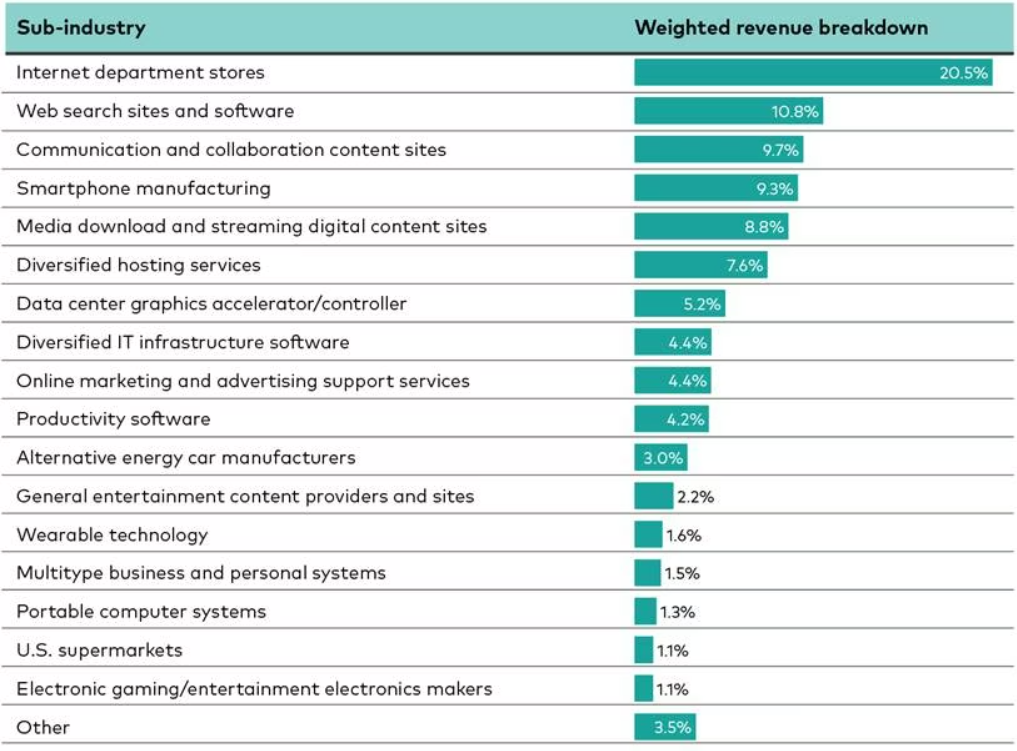

The Magnificent Seven business models span how we work, play, and consumeSources of the companies' combined 2025 revenues of $2.2 trillion

Notes: Weighted revenue breakdown is the proportion of combined revenues attributed to a given source. It is determined by aggregating the revenue from each source across companies and then dividing this figure by the total revenue from all companies combined. Revenues are based on the company’s reported annual fiscal year total revenue for 2025. Sum may not total 100% due to rounding. Sources: Vanguard calculations, based on data from FactSet, as of January 2026.

Consider a few examples:

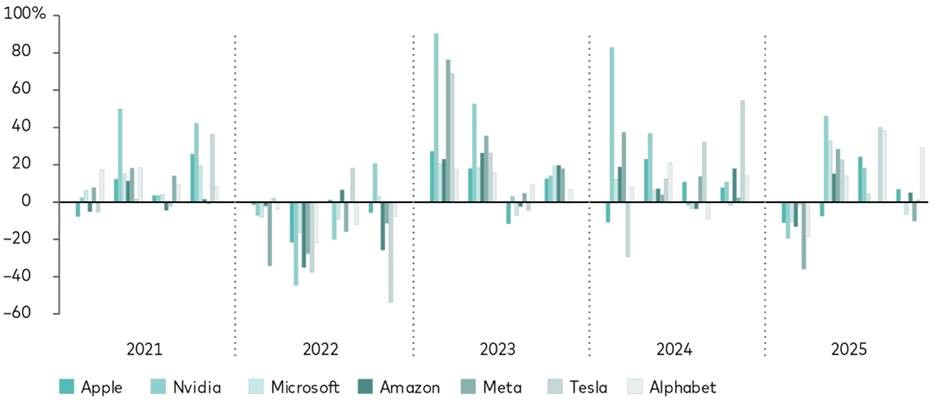

While all three companies serve both consumers and commercial clients, their revenue exposures vary meaningfully across and within each company. “The diverse revenue sources matter because they show that the Magnificent Seven’s business models span different end-users and markets,” said Erich Pingel, an analyst in Vanguard Investment Strategy Group. “Differences in business models also mean differences in risk-factor exposures, which helps explain why their stock prices do not move entirely in lockstep.”

The Magnificent Seven stocks have not moved in lockstepQuarterly total returns of common stocks, Q4 2020-Q4 2025

Sources: Vanguard calculations, based on data from FactSet, as of December 31, 2025.

Seven stocks: Neither narrow nor self-contained“The Magnificent Seven currently represents around 30% of the U.S. stock market. The companies are often portrayed as a monolith, but their business models tell a different story,” said Rodney Comegys, chief investment officer, Vanguard Capital Management, and head of Global Equity. “Their commercial and equity market success coexists with meaningful differentiation at the company level—making it unlikely that all of them will disappear or experience significant drawdowns at the same time. They share a label, not a business model.” For investors with long time horizons, it’s worth considering how creative destruction—the process by which innovation disrupts products, technologies, and companies—recasts market leadership. Comegys said that those inclined to consider the market’s evolution over short periods should recognize that market leadership often changes—and that the human tendency to expect trends to persist is just one factor that makes it hard to predict who the new winners or laggards will be or when the transition happens. The world is more interconnected and interdependent than ever, due in no small part to technological progress. Although the Magnificent Seven share common elements, the companies and their stocks are not interchangeable. Their business models, strategies, and consumer bases vary—and so has the performance of their stock prices.

Vanguard |